Why KCLI / APCOF Is Now My Largest Holding (And still undervalued)

In less than a year American Critical Minerals has transformed from dormant asset to a funded, institutional-grade development story backed by a blue chip team. Share price is spring loaded.

American Critical Minerals Corp.

CSE: KCLI / OTCQB: APCOF / Frankfurt: 2P3

Market capitalization: $20.3M CAD

On April 27th I referred to KCLI as “one of my largest” junior exploration holdings.

The share price has, as Rick Rule often puts it, “delightfully” remained in the low $0.20s, as the broader market continues to overlook what’s developing here.

Thanks to a low share price, today it is my largest holding.

It’s been a few months since I provided a thorough update on American Critical Minerals, but events over the past few weeks warrant another serious look.

Before we get into the details, a word on how I think about Simon Clarke, who recently moved from CEO to Executive Chairman.

Simon founded Osum Oil Sands, built it to 20,000 bpd before a ~$400M sale to Waterous Funds in April 2021.

He also helped grow American Lithium to its position of being one of the largest lithium development companies globally with 2 advanced stage, large scale lithium projects, helming it to a market valuation of approx. $1.2 billion.

When his associates brought the KCLI opportunity to his desk and walked him through the details, he took his time.

At that time, the story was buried so deeply under the radar because of a decade of permitting hell, it sat at a minuscule valuation and hardly traded.

What Clarke saw was enough to get him to come on board and direct the company toward its next phase: becoming America’s next potash and lithium mine.

In a comprehensive April interview with TriAngle Investor, Simon said: “we’re moving toward becoming an institutional play.”

Over the last 9 months, Clarke has deftly assembled a leadership team that can easily rival any blue chip in the sector. More on that below.

More recently, the catalysts have stacked significantly in our favor, and the company is on the cusp of what its longest-term institutional investors have been waiting on for over a decade.

At a $20M CAD market cap, the opportunity is unprecedented and this is what investors are overlooking.

What KCLI Actually Is

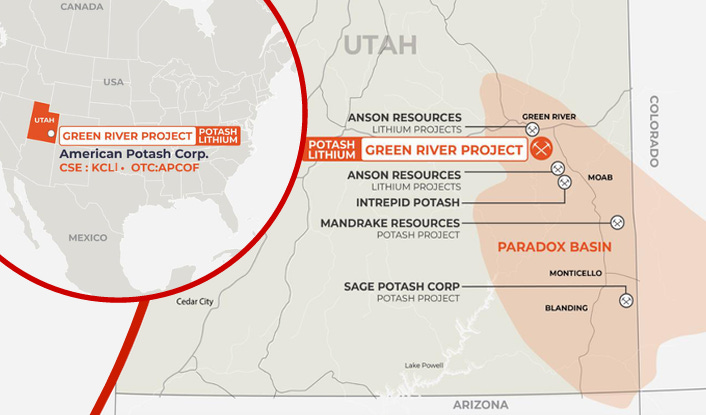

American Critical Minerals controls 32,530 acres in Utah’s Paradox Basin, the only Super Basin in America.

The property hosts potash, lithium, and bromine across a single massive brine system.

The lesser known mineral, bromine, has strong macro tailwinds and for KCLI will act as a credit toward cash flow that lowers operating costs.

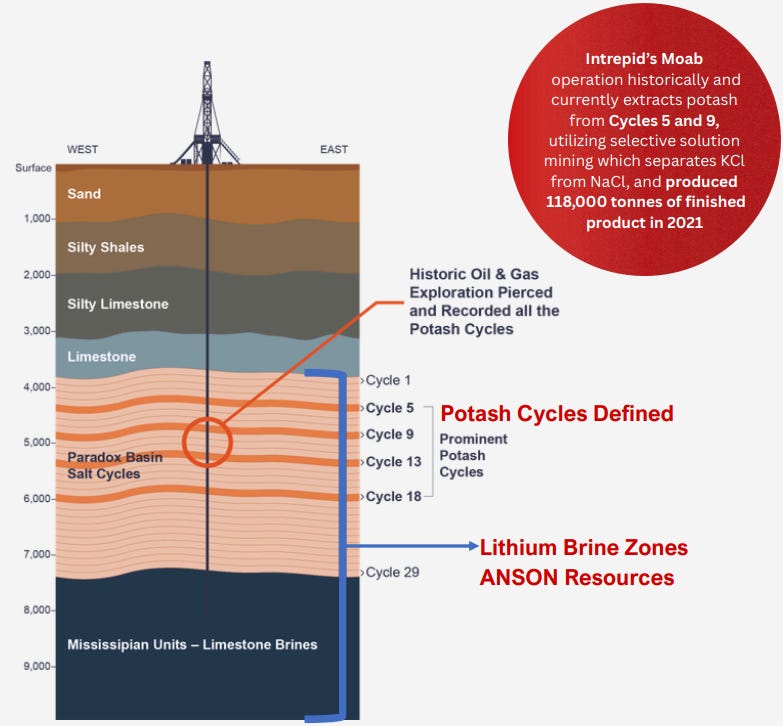

Intrepid Potash (NYSE: IPI) operates just 20 miles away and has mined the same Cycle 5 formation for over 60 years.

Anson Resources sits adjacent to KCLI on two sides, developing its lithium resource with a completed feasibility study, a Koch DLE partnership, Korean industrial giant POSCO funding a large-scale pilot plant, and an LG Energy Solution offtake agreement.

KCLI’s project has already been de-risked by its neighbors, without the company spending a dime.

In a recent interview with Jesse Day (Commodity Culture), CEO Dean Pekeski put his geological confidence plainly: “The fact that we’re only 20 miles from their (Intrepid Potash’s) location, really in the shadow of their headframe, gives us confidence that we’re going to encounter the same geology that they’re mining in our area. In fact, we know that to be the case.”

This has long moved from speculation to a ticking time bomb waiting for KCLI to drop its first deep drill hole.

That happens in 4-6 weeks.

The geology has been proven by Intrepid Potash, Anson Resources, and most importantly for KCLI, by data from 22 historic oil and gas wells on their own property, loaded with valuable seismic intel.

Internationally renowned engineering firm Agapito Associates, who constructed KCLI’s NI 43-101 Large-Scale Exploration Target, says there is significant potash, lithium and bromine down there. Tens of billions of dollars worth.

Pekeski confirmed in his interview that historic oil and gas logs show up to 6 metres grading ~29% KCl - “mine-grade” as he put it - squarely in line with Intrepid’s producing mine.

On the lithium side, the same logic applies. “From a proximity perspective, we know that the formations Anson Resources is intending to mine, extend onto our property. We’ve got seismic data that shows those beds exist at depth.”

Macro tailwinds are strong

The macro backdrop for all three commodities is the strongest it has been in years.

Russia banned ammonium nitrate exports earlier this year and the U.S. imports 96.5% of its potash, leaving American farmers exposed to geopolitical supply shocks.

Canaccord Genuity projects a lithium deficit through 2035, driven by Chinese production shutdowns, Australian mine curtailments, and re-accelerating demand from EVs, battery storage, and electric trucks.

Bromine supply remains concentrated in China and the Dead Sea region, with limited Western production despite growing demand from HVAC absorption chillers, flame retardants, and water treatment.

Both potash and lithium sit on the USGS Critical Minerals List, and KCLI is positioned to become a domestic source for all three.

THE PULSAR HELIUM PLAYBOOK ALL OVER AGAIN

Pulsar Helium (TSXV: PLSR / OTCQB: PSRHF) is a textbook example of what KCLI investors are looking forward to.

Pulsar crossed my desk when it went public in mid-2023 at $0.30.

I picked up coverage long before the market caught on.

The Ambient Noise Tomography (ANT) graphics told the story before any drill bit turned.

The highest-grade primary helium on the planet was right there, in the heart of Minnesota. All Pulsar had to do was sink a drill into it to prove it to institutional investors.

Pulsar drifted at $0.45-$0.75 for nearly two years. In October 2025, the drill hit.

The stock ran from $0.45 to $1.20 in two weeks, then continued appreciating to $2.69 as the discovery developed and de-risked.

KCLI sits at that exact inflection point right now.

What I saw in Pulsar’s ANT graphic, I see in KCLI’s Paradox Basin Cycle cross section - the paydirt is there, and it’s huge.

The company is constructing its first drill pad on the property as you read this.

The geology is known. All that’s left is to drill that first hole in August, over a decade in the making.

A Team Built to Build a Mine

Dean Pekeski stepped into the CEO role in March.

He has 20 years of potash-specific experience, having taken Western Potash’s Milestone project through full permitting and Peak Minerals’ Utah brine project to feasibility.

Simon Clarke, as mentioned earlier, moved to Executive Chairman to drive capital markets activity and institutional positioning.

Kenneth Taylor, former Executive VP of Business Development at NYSE-listed Intrepid Potash, advises the company on solution mining and Utah-specific operational matters.

Eric Miller sits on the board as a former first U.S. representative for Canada’s Department of Industry, a Global Fellow at the Woodrow Wilson Center, and an advisor to governments and mining companies globally on critical minerals policy for over 20 years.

Pekeski confirmed in the Jesse Day interview that federal funding discussions are already underway: “We’re also exploring opportunities with various U.S. government agencies right now to better understand what funding options might be available to the company through federal support.”

We are witnessing a $20 million market cap company that has assembled a blue chip institutional-grade team to execute a technical program in a proven basin.

What’s Happened in the Last Few Months

RESPEC has been engaged for drill execution. They have overseen and managed 39 procurement programs in the Paradox Basin, where KCLI’s Green River asset is situated.

From my April 27th update: “The Paradox Basin isn’t for amateurs. These are deep, technical programs requiring engineering discipline and operational credibility institutions can underwrite.”

When RESPEC gets involved in a project of this magnitude, institutions pay attention. Nobody knows how to plan and execute a complex deep drill program in this basin better than them.

Red Cloud Securities initiated coverage on April 24, calling first drill results “the primary catalyst for rerating.”

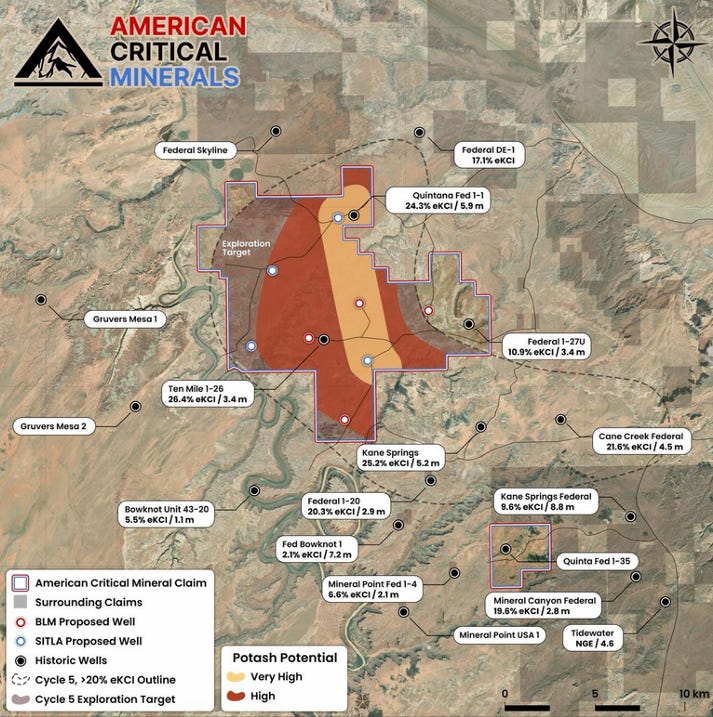

Field crews mobilized on June 22 and drill pad construction is underway at Duma Point AP-S-02, located immediately adjacent to the historic well that returned 24.3% eKCl over 5.9 metres, the highest historical grade encountered anywhere on the property.

In an effort to top up the treasury without further share-based dilution, the company recently announced a warrant exercise accelerator program. That overhang is now gone, with the cutoff date being June 28.

The Size of the Prize

The Agapito-constructed 43-101 large scale exploration target outlines 500-950 million tonnes of potash, 600,000-1.7 million tonnes of lithium carbonate equivalent, and 3.3-9.1 million tonnes of bromine.

At current commodity prices, in-situ value ranges from $50.7 billion (bear case) to $144.6 billion (bull case).

The bromine component alone contributes between $13.2 billion (bear case) and $36.4 billion (bull case) of that in-situ value at current prices.

Apply brutal recovery and risk discounts, you still land at multi-billion-dollar in-ground economic value.

Current enterprise value sits at ~$12.5M CAD.

Red Cloud’s peer average is $103.5M CAD.

KCLI trades at 12% of peers.

My Take

I build large positions in my portfolio that are justified not only by the geology, but by management teams that have successfully proven they are capable of delivering what they say they will deliver.

The market is still pricing KCLI as a concept, primarily because it remains under the radar of the larger (primarily American) institutional capital looking to fund large-scale projects.

Chairman Simon Clarke has expertly turned KCLI into an institutional-grade company.

The Pulsar setup is nearly identical to KCLI here.

The gap between today’s greenfield valuation and institutional-grade brownfield developer with these boxes checked has historically closed in multiples, not percentages.

Haywood Securities kept the lights on and property in good standing for a decade, because they knew that when the permits cleared and the team was in place, it would be time for this plane to take off.

That time is now.

I believe we are in the final stretch before cheap shares are no longer available.

IMPORTANT DISCLAIMER AND RISK DISCLOSURE

This analysis is provided for informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or a recommendation to buy, sell, or hold any securities. The author is not a licensed financial advisor, investment advisor, broker-dealer, or registered investment advisor and does not provide personalized investment advice or recommendations tailored to any individual’s financial situation.

All information presented is the author’s opinion based on publicly available information and should not be relied upon as the sole basis for any investment decision. Readers should conduct their own due diligence, research, and analysis before making any investment decisions and should consult with qualified, licensed financial professionals before investing.

Junior mining and exploration stocks carry substantial risks, including but not limited to: potential total loss of investment, extreme price volatility, liquidity risk, operational risks, regulatory changes, commodity price fluctuations, exploration failures, and dilution from future financings. These investments are speculative in nature and may not be suitable for all investors.

The author may hold positions in securities mentioned and may buy or sell such positions at any time without notice. Past performance does not guarantee future results.

Forward-looking statements and projections are inherently uncertain and subject to numerous risks and uncertainties. Actual results may differ materially from any projections or expectations expressed herein.

This content is not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to local law or regulation. By reading this analysis, you acknowledge that you understand and accept these risks and limitations.