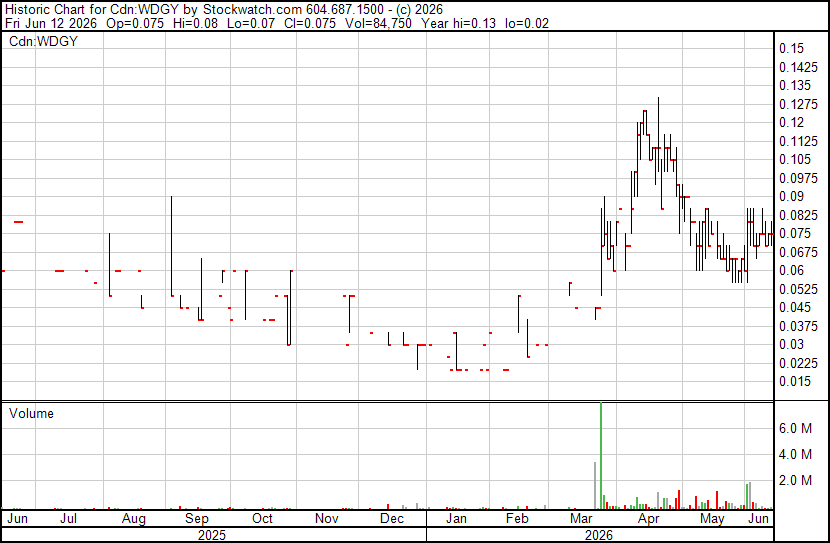

JMP SPECIAL: Wedgemount Resources (CSE: WDGY / OTCQB: WDGRF)

Permian Basin oil production ramping. Uranium and REE breccia pipes adjacent to Energy Fuels Pinion Plains. $7 million market cap? Wake me up.

Wedgemount Resources is a $7 million market cap company with a producing and rapidly growing Permian Basin oil field targeting 5,000 BOE/D across 22,000 acres in Texas, and a freshly optioned district-scale uranium and rare earth project in Arizona sitting directly adjacent to Energy Fuels’ Pinyon Plain Mine, the highest-grade producing uranium operation in the United States.

Either asset alone, in my view, is worth multiples of today’s market cap, right now.

The market forgot about WDGY. But they’ve rebooted, cashed up and are marching ahead - with or without investors attention.

Together, in one vehicle, at this price, I think you back the truck up and load it.

The oil field: 125 BOE/D today, 5,000 BOE/D capacity

The Permian Basin operation is live and ramping.

Current production sits at 125 BOE/D, ahead of internal projections, with a Q4 2026 target of 500 BOE/D.

The company owns 131 vertical production wells and 14 injectors across 22,000 acres in Runnels and Coleman counties, Texas, on the conventional Eastern Shelf of the Permian Basin. 100% working interest.

A 24-hour compliance test across all wells came in at 841 BOE/D, 80% light oil and condensates.

The wells produce. The reservoir delivers. What’s been missing is capital to optimize surface facilities and bring wells back online in sequence.

That’s now happening.

The company recently closed a $1.25 million oversubscribed financing and immediately deployed it into a phased reactivation program.

Phase 1 (Crews and Talpa, 22 wells including their best producers) is already delivering. Phase 2 targets 62 wells on the Echo field that have never been optimized. Phase 3 brings on another 41 wells at Novice. Each phase builds cash flow that funds the next.

Beyond optimization, over 300 undrilled locations on 40-acre spacing provide the runway to 1,000, 2,000, and ultimately 5,000 BOE/D.

At that production rate and $80 oil, you’re looking at a mid-tier producer generating north of $100 million CAD in annual free cash flow.

Management has been clear: the reservoir supports it. It’s a matter of staging capital and keeping the share count tight.

Skin in the game

CEO Mark Vanry and CFO Steve Vanry personally funded this company through the downturn, lending over US$400,000, buying $505,000 in convertible debentures, and advancing additional capital interest-free.

They kept the lights on with their own money through pipeline outages, brush fires, and sub-$70 oil because they know what this asset is worth on the other side.

At 500 BOE/D and $80 oil, my base case estimates roughly $15 million in free cash flow on today’s $7 million market cap. At 1,000 BOE/D, estimated free cash flow approaches $32 million.

The uranium play: this is where it gets extraordinary

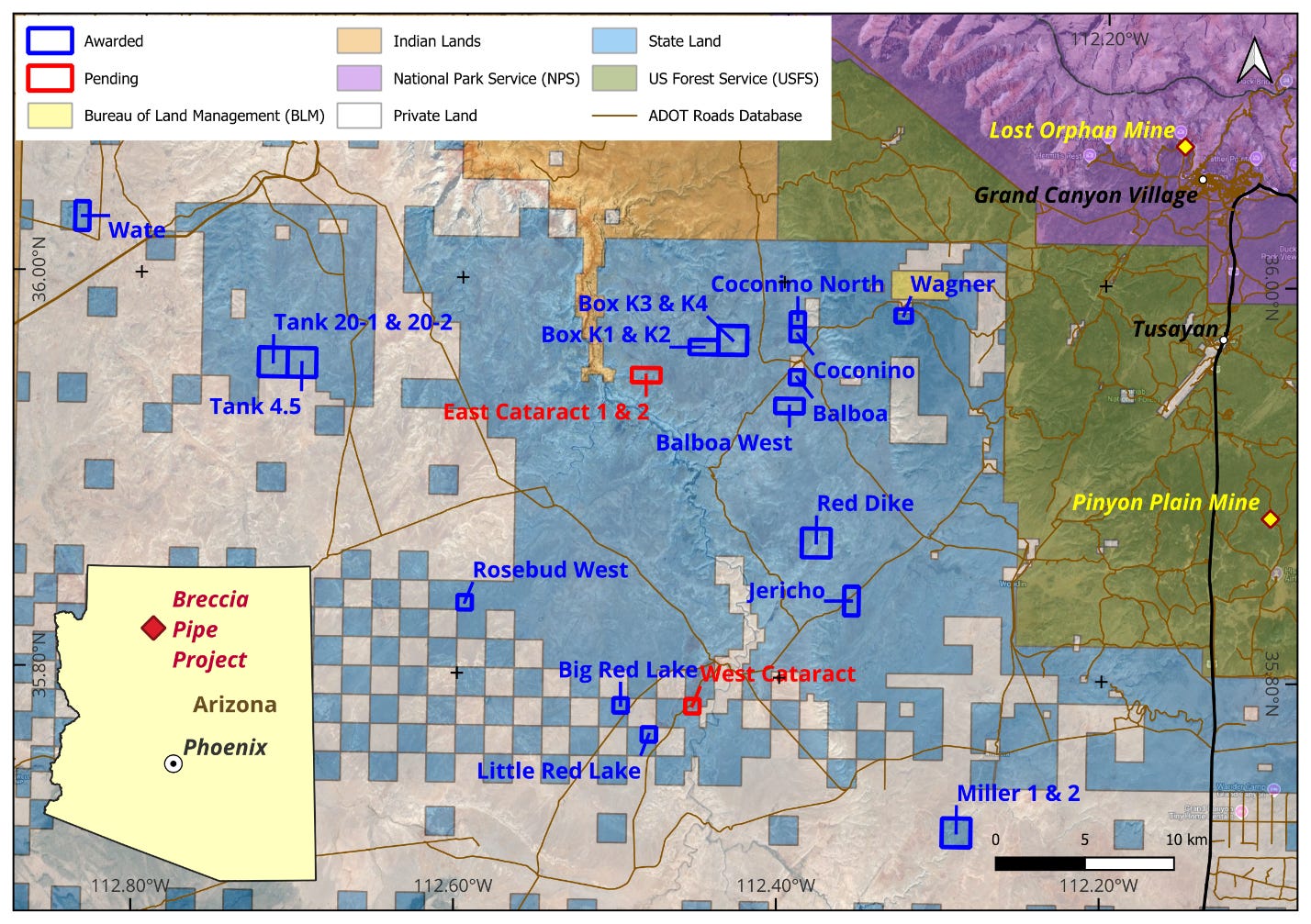

On June 9th, Wedgemount optioned 23 breccia pipe uranium and REE targets from Myriad Uranium across 5,600 acres in Northern Arizona’s legendary Arizona Strip district.

This is a concentrated package of targets in the highest-grade uranium district in the United States, anchored by a deposit that was formerly owned by one of the largest uranium producers on the continent.

What are breccia pipes???

A geology so unique, so rare, and very profitable when mined. WDGY scored big here. Let’s unpack this.

Beneath the Colorado Plateau, massive limestone formations contain caverns.

When those caverns collapse, they create vertical cylinders of broken rock that drop over a thousand feet into the earth.

These columns are permeable, which means fluids move through them, and over geological time, uranium concentrates inside at grades you almost never see in conventional deposits.

Picture a narrow, high-grade chimney of ore, 200 to 400 feet across and hundreds of feet deep, requiring less than 20 acres of surface disturbance to mine.

They’re compact. They’re rich. And they’re a completely unique animal in the uranium world.

The Arizona Strip produced over 23 million pounds of U3O8 through the 1980s.

This is proven ground.

The crown jewel in Wedgemount’s package is the Wate Pipe, formerly owned by Energy Fuels.

It carries a historical resource estimate (SRK Consulting, 2015, not current under NI 43-101) of 71,000 tons containing 1.12 million pounds eU3O8 at an average grade of 0.79%.

That’s a deposit with over a million pounds of uranium already delineated, sitting in a district with active production and existing processing infrastructure.

Now look next door.

Energy Fuels’ Pinyon Plain Mine sits in the same geological district, same deposit type, same formation.

Pinyon Plain’s pre-feasibility study estimated grades of 0.58%.

Actual mined grades have demolished that estimate: 2.23% average in Q2 2025, peaking at 3.51% in June 2025 alone.

That means the ore coming out of the ground was six times richer than the engineers originally modeled.

Energy Fuels’ White Mesa Mill in Utah, the only operating conventional uranium mill in the United States, provides regional processing infrastructure.

Pinyon Plain runs directly into Wedgemount’s ground.

Wate’s historical grade of 0.79% is already higher than Pinyon Plain’s pre-mine estimate. And there are 22 additional targets behind it, most of them underexplored, in a district that keeps outperforming expectations.

Published technical literature has also noted rare earth element enrichment in some Arizona breccia pipe systems.

If confirmed on Wedgemount’s targets, that adds a critical minerals dimension to an already compelling uranium story.

The strategy: two engines, one vehicle

I view this as a calculated move to build a diversified American energy company with two distinct value-creation engines.

Myriad Uranium, which holds one of America’s most coveted uranium development assets at its Copper Mountain project in Wyoming, knows the uranium business better than most.

They chose to do business with Wedgemount by optioning the Breccia Pipe Project under a structure that keeps Myriad’s skin in the game at up to 50% ownership.

Wedgemount can earn up to 75% over three years for US$75,000 cash, staged share issuances, and C$4 million in exploration spending.

The vision is elegant. Oil and gas cash flow from the Permian funds uranium exploration in Arizona.

Both assets sit in the most operator-friendly jurisdictions in North America, during an administration pushing energy dominance, with Russian uranium imports banned and AI-driven power demand creating a structural supply deficit in both hydrocarbons and nuclear fuel.

Mark Vanry called this “a defining moment for Wedgemount as we become a diversified energy provider in the USA.”

I agree.

The valuation

At $7 million market cap, you are getting a Permian Basin oil field generating growing cash flow with a realistic path to $100 million in annual revenue, plus a district-scale uranium project adjacent to a $3+ billion producer pulling some of the highest-grade ore on earth.

The Wate Pipe alone hosts a historical resource of over a million pounds of uranium.

I cannot find another public company offering this combination at this price.

IMPORTANT DISCLAIMER AND RISK DISCLOSURE

This analysis is provided for informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or a recommendation to buy, sell, or hold any securities. The author is not a licensed financial advisor, investment advisor, broker-dealer, or registered investment advisor and does not provide personalized investment advice or recommendations tailored to any individual’s financial situation.

All information presented is the author’s opinion based on publicly available information and should not be relied upon as the sole basis for any investment decision. Readers should conduct their own due diligence, research, and analysis before making any investment decisions and should consult with qualified, licensed financial professionals before investing.

Junior mining and exploration stocks carry substantial risks, including but not limited to: potential total loss of investment, extreme price volatility, liquidity risk, operational risks, regulatory changes, commodity price fluctuations, exploration failures, and dilution from future financings. These investments are speculative in nature and may not be suitable for all investors.

The author may hold positions in securities mentioned and may buy or sell such positions at any time without notice. Past performance does not guarantee future results.

Forward-looking statements and projections are inherently uncertain and subject to numerous risks and uncertainties. Actual results may differ materially from any projections or expectations expressed herein.

This content is not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to local law or regulation. By reading this analysis, you acknowledge that you understand and accept these risks and limitations.