Data Centers Are Eating Indium; War Is Eating Tungsten; Gold Is Bulling Along. GoldHaven Has It All.

Two of the world's tightest commodities (not copper). Two drill programs (including Phase 2 on a Brazilian gold asset). GoldHaven (CSE: GOH, OTCQB: GHVNF) market cap: $13 million.

Shares of GoldHaven Resources have dipped from a March 1 high of 0.38/share to close at 0.29 today, bringing its market cap down to $13.5M.

In this article I explain why I am strategically adding to my position at this level.

Technical Setup: GOH has pulled back ~24% from its March 1 high of $0.38, consolidating in the $0.28-$0.31 range on declining volume. This is a textbook cooldown after a 200%+ breakout from the $0.12 base that held from October through December. March 17 saw the heaviest sell volume (525K shares) with an intraday low of $0.27 that was immediately bought; followed by a volume low (127k) on March 17th, not seen since January 5th. This is a classic a shakeout candle. This kind of consolidation typically precedes a second leg higher when catalyst start hitting.

Indium is the resource world’s secret weapon - overnight. Data Centres and AI tech cannot run without it. But there are no indium mines on earth - it’s a mineral produced as a bi-product of zinc.

War is eating up America’s tungsten supply, causing the Pentagon to scramble (The U.S. has not mined tungsten since 2015)

GoldHaven has found high grades of all three in BC.

Every AI laser chip starts with indium phosphide.

The indium supply chain is all of a sudden in a 70% deficit thanks to the data centre surge overtaking the planet.

GoldHaven’s Magno just lit up with indium-enriched zinc at 3,000x crustal background, and a financed drill program is about to test the porphyry system driving it.

GoldHaven Resources Corp.

CSE: GOH | OTCQB: GHVNF | FSE: 4QS

Market Cap: C$13.97M

30 Second Thesis

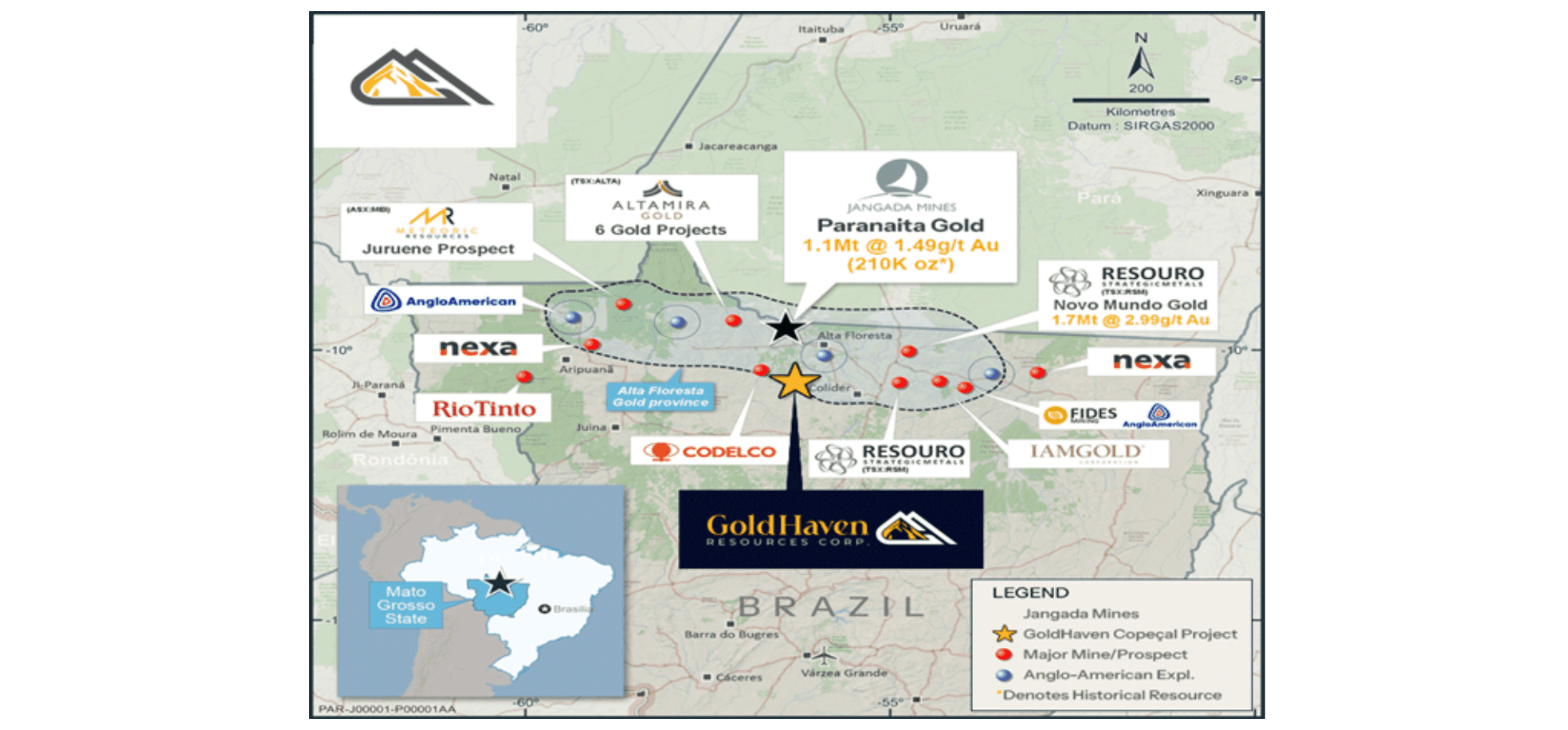

GoldHaven controls 37,200 hectares at Magno in BC’s Cassiar district, directly adjacent to blue chip Coeur Mining’s producing Silvertip mine and Cassiar Gold’s $79M exploration play.

Last years surface sampling has confirmed a rich six-metal system (tungsten, indium, gallium, copper, silver, zinc) with classic porphyry zonation pointing to something large and untested at depth.

My accumulation target remains between $0.28 and $0.35 ahead of a $2M flow-through financing (no warrants! = no future overhang) that funds 3D geological modeling, geophysics, and drill permitting.

Why I am still accumulating shares? Two of GoldHaven’s six metals became front-page commodities this year. Demand is not going away any time soon.

To be clear – Magno will not be a mine in the near future. But if the geological thesis holds, it will become extremely important to: China, U.S., Canada and other countries angling for indium, tungsten and copper…. with a silver kicker thrown in for good measure.

Play #2: Gold in Brazil… The Sizzler.

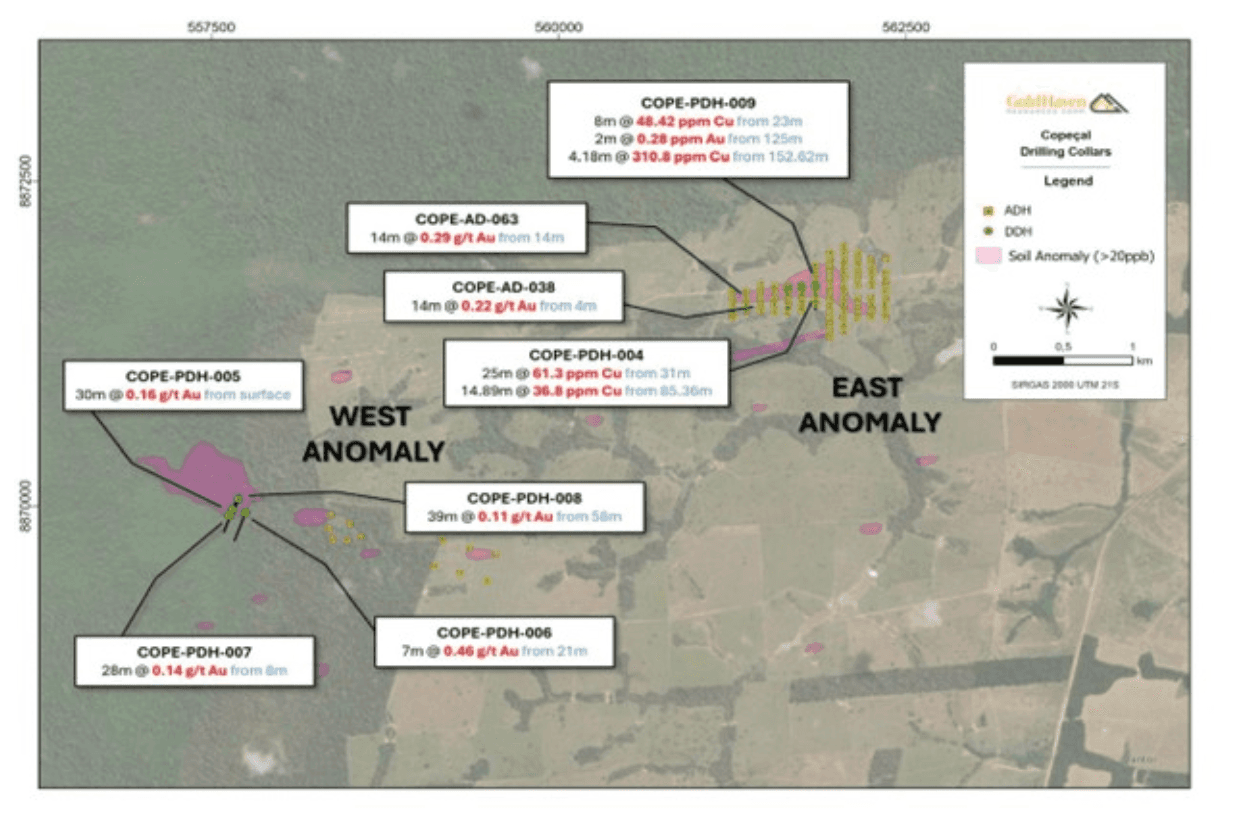

Today, GoldHaven released results from their maiden drill program at Copecal in Brazil. Nine holes completed across two targets.

The West Target emerged as priority with gold in both the weathered surface layer and bedrock, quartz veining, and structural features pointing to a larger mineralized system.

Phase 2 drilling is planned for mid-Q2 2026.

At $5,000 gold and Tocantinzinho-equivalent geology 150km away, Copecal is a free lottery ticket with a legitimate shot at a violent re-rate.

We’re positioning for TWO drill programs this year with a catalyst rich Spring/Summer season ahead.

The macro section (skippable, but important)

I’m not pitching GoldHaven as a “hot commodity price” play. We don’t play that game around here.

The stock revalues on what the drill bit finds.

That said, the macro context explains why capital and government attention are flowing into this space, and why strategic buyers will eventually care about Magno.

Tungsten is up 557% since China imposed export controls in February 2025. Bloomberg reported this weekend that BMO’s head of commodity research has “never seen a market as tight as tungsten is right now.”

Tighter than copper? Way tighter.

Chinese shipments of restricted tungsten products dropped 40% last year.

The Pentagon is scrambling for supply. The US hasn’t mined tungsten commercially since 2015, and military consumption is set to rise 12% this year as the Middle East conflict burns through munitions.

Shell Canada confirmed tungsten at depth on GoldHaven’s Magno property in the 1980s – now it’s time to attack these anomalies with today’s technology.

Indium just collided with the AI infrastructure buildout.

Nvidia recently invested $4 billion into two photonics companies in March 2026 to lock up laser chip supply for AI data centers.

Those laser chips are built on indium phosphide substrates, and the industry is running a 70% supply deficit.

Indium is only recovered as a byproduct of zinc smelting.

China controls 70% of supply and slapped export licensing on it in February 2025.

This genuinely appears to be a structural shortage, not a speculative spike.

Military consumption of tungsten (helicopters, fighter jets, armor-piercing ammunition, missile components) is set to rise 12% this year.

The US hasn’t mined tungsten commercially since 2015 and new Western supply is at least two years away.

A Canadian government publication states Canada could supply 100% of current US tungsten needs.

Indium: the AI photonics metal.

Indium is recovered exclusively as a byproduct of zinc smelting, making supply inelastic to price.

Spot pricing sits around $580-640/kg (highest in a decade). Chinese unwrought indium exports fell 23% in December 2025.

The US Defense Logistics Agency issued a $125M solicitation for high-purity indium ingots in January 2026.

Indium has nearly overnight become the new hotshot mineral in town becuse silicon photonics is replacing copper wiring for high-speed data transmission inside AI data centers.

The laser chips that make it work are built on indium phosphide, a compound semiconductor made from indium and phosphorus.

Silicon can guide light but it can’t generate it. For that you need InP.

The problem: global InP device demand hit 2 million pieces in 2025 against production capacity of 600,000. A 70% gap.

Orders at major InP substrate suppliers (there are only 2-3 at scale globally) are fully booked through 2026. Lead times for laser components have been pushed past 2027.

None of this changes the fact that indium only comes from zinc mining.

Both metals sit on US and Canadian critical minerals lists and the macro ensures capital flows into exploration.

What does The Rock say?

The January 29th data release summarized what CEO Rob Birmingham calls “a large, zoned, intrusion-related system.”

GoldHaven’s 357 surface samples show systematic metal transitions across the property.

Lead-rich carbonate replacement deposits at the edges. Zinc-tungsten-dominant skarns closer to the center. Copper elevated up to 6,660 ppm in the granite itself.

This is the geological fingerprint of a porphyry intrusion at depth acting like an industrial furnace, pumping metal-rich fluids outward through the surrounding rock.

As those fluids cool and travel away from the source, different metals precipitate at different temperatures.

Lead and silver drop out first (cooler, farther). Tungsten and zinc closer in (hotter).

Copper and molybdenum at the core.

When you see this zonation across 37 square kilometers, you know the system is big.

The 11,000+ meters of historical drilling never tested this interpretation – they didn’t know how to.

Geologists in the 1950s-1980s drilled individual showings in isolation.

GoldHaven is reprocessing that data to target the system as a whole.

The NI 43-101, filed March 6 by independent QP James Turner P.Geo., validates stacked deposit environments (copper-gold, silver-lead-zinc carbonate replacement, tungsten-skarn, and critical mineral targets) within one interconnected system.

The question is whether drilling confirms the scale and grade continuity the surface geochemistry suggests.

Nobody has drilled Magno with a modern porphyry model. That changes this year.

The Brazil wildcard: Copecal assays call for Phase 2 initiation

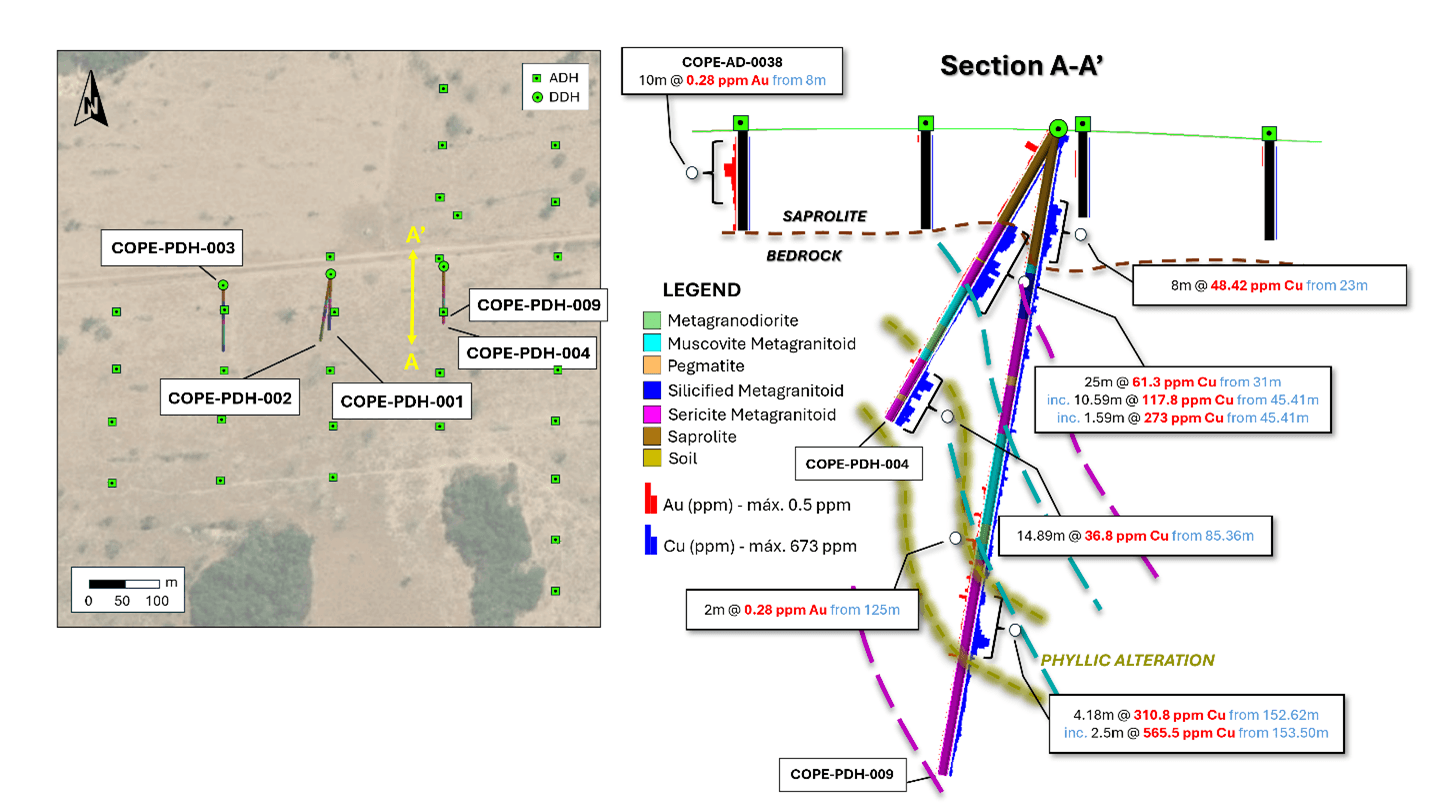

Today’s press release confirms GoldHaven completed all nine holes of their maiden diamond drill program at Copecal.

First-ever drilling on the property, with two intriguing targets tested.

The West Target is the clear winner.

Gold showing up in both the weathered surface layer and the hard rock underneath, with quartz veining and structural features that point to a larger mineralized system at depth.

Saprolite extends to 60 meters, which suggests preferential weathering along structurally controlled alteration zones.

Phase 2 drilling is now planned for mid-Q2 2026, focused entirely on vectoring into the higher-grade core.

The East Target hit gold and copper with alteration consistent with intrusion-related systems. The interpretation: these holes caught the outer edge, not the center.

That’s actually constructive intel. If you’re on the fringe, the hotbed of activity is nearby and untested.

East Target sulphide assays are still pending. Thirty meters of chalcopyrite-pyrite plus the first-ever bornite encountered at Copecal.

Separate catalyst, coming soon.

Same host rock geology as Tocantinzinho’s 2 million ounce deposit ~150km away.

If Phase 2 holes hit 20-30 meters @ 0.5-1.0+ g/t, Copecal becomes a legitimate discovery

Meaning, that combination works at scale in Brazilian open-pit settings, and there will be a mandatory shock-rerate on the stock.

This is a different animal than when AngloGold was exploring at $1,800.

Catalyst calendar

Near-term (weeks): East Target sulphide assays from Copecal. 30m chalcopyrite-pyrite plus first-ever bornite. Could be a significant re-rate.

Mid-Q2 2026: Copecal Phase 2 drilling. West Target follow-up vectoring into higher-grade zones.

Q2-Q3 2026: Magno drill program. First-ever drilling on a property with confirmed high-grade six-metal mineralization. The main event.

Ongoing: 3D geological modelling and target refinement at Magno.

Risk assessment

Exploration risk. Grab samples are not resource estimates. Drilling could underperform surface geochemistry.

Single-asset concentration. The thesis hinges on Magno delivering. If drilling disappoints, the $14M cap has room to fall.

Dilution. Future drill programs require additional capital.

Commodity sensitivity. A relaxation of Chinese export controls could cool sentiment.

Timeline. A mine at Magno is years away. This is discovery-stage optionality.

Actionable intel

GoldHaven sits at the intersection of district-scale discovery potential, a six-metal critical minerals portfolio, and imminent, consistent near term catalysts from two continents.

Two drill programs are now firing through summer.

Copecal Phase 2 mid-Q2 targeting the core of a confirmed mineralized system at $5,000 gold.

Magno Q2-Q3. First-ever drilling on a property showing porphyry signatures across six metals with a producing mine next door.

Tungsten is posting a historic rally on munitions demand and supply panic.

The AI photonics buildout is creating a new structural demand vector for indium.

Western governments are throwing billions at critical mineral supply security.

The stock has dipped and consolidated at the 0.28-0.31 level.

If the drill bit delivers what the surface geochemistry suggests, the risk/reward at this market cap, in my opinion, is well positioned in our favor.

IMPORTANT DISCLAIMER AND RISK DISCLOSURE

This analysis is provided for informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or a recommendation to buy, sell, or hold any securities. The author is not a licensed financial advisor, investment advisor, broker-dealer, or registered investment advisor and does not provide personalized investment advice or recommendations tailored to any individual’s financial situation.

All information presented is the author’s opinion based on publicly available information and should not be relied upon as the sole basis for any investment decision. Readers should conduct their own due diligence, research, and analysis before making any investment decisions and should consult with qualified, licensed financial professionals before investing.

Junior mining and exploration stocks carry substantial risks, including but not limited to: potential total loss of investment, extreme price volatility, liquidity risk, operational risks, regulatory changes, commodity price fluctuations, exploration failures, and dilution from future financings. These investments are speculative in nature and may not be suitable for all investors.

The author may hold positions in securities mentioned and may buy or sell such positions at any time without notice. Past performance does not guarantee future results.

Forward-looking statements and projections are inherently uncertain and subject to numerous risks and uncertainties. Actual results may differ materially from any projections or expectations expressed herein.

This content is not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to local law or regulation. By reading this analysis, you acknowledge that you understand and accept these risks and limitations.